Blockchain has revolutionized the transfer of value and allowed anyone not only to participate without permission but also to innovate without permission. The result has been a wild flourishing of different forms of tokenized value, and the birth of an industry — decentralized finance, or “DeFi”.

Why is DeFi better than traditional finance? Why don’t you just get your interest from a bank? Defi does not just take existing centralized finance concepts and make them available to the masses — it allows for entirely new applications to be imagined and created. Consider this. You place money into a contract that is not owned by anybody, then an autonomous software bot takes that money and uses it to take out a massive loan, performs complicated arbitrage operations for profit, and repays the loan in a fraction of a second at no risk. It splits the profits not with bankers, but between you and other depositors. Sounds Futuristic? Well, the future is here.

With the emergence of many similar DeFi protocols, the opportunities for savvy investors grew exponentially. By lending to one protocol, then staking the rewards somewhere else, APY could be amplified. This is the essence of a new phenomenon known as yield farming and the process could even be repeated with borrowed funds, creating a high-risk high-reward strategy. A developer named Andre Cronje decided there must be a way to automate this, and in doing so created Yearn Finance, which is one of the most successful DeFi projects with the value locked around 400 million USD.

Putting your funds to work – outdated

Traditional banks take custody of your funds, and while doing so, lend them out for interest to the next customer. This customer spends that money with someone else, who then deposits it, enabling it to be lent out again. So, $1 deposited in the original bank has “created” several more dollars in a process known as fractional reserve banking. The bank of course takes its own cut, and the depositor might receive a small amount per annum (APY — annualized percentage yield), perhaps a single percent if they are lucky. These days however depositors are more likely to actually pay a small fee for the privilege of providing liquidity through their savings since the interest rates are close to zero or minus hence the system is broken.

Putting your funds to work – new era

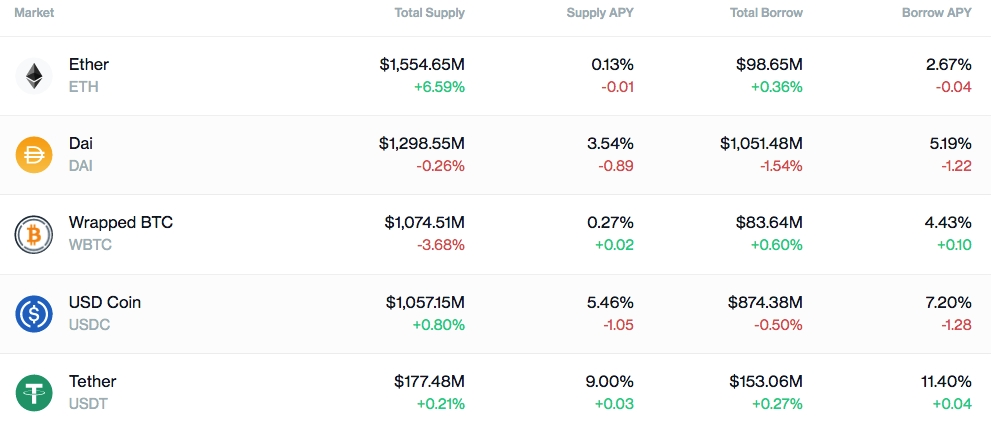

Peer-to-peer finance changes this. Users interact directly with protocols: no bank takes a cut. Liquidity is provided with no third-party involvement. How does this work? The depositor places funds directly into a smart contract hence it acts like a bank. Most of the contracts are audited by credited and well-known tech companies to mitigate the risks. Earnings of supply or borrow APY see in the picture below.

Most Defi borrowing platforms require collateral to be deposited in order to borrow. For example, to borrow 50 ETH, you may need to deposit 100 ETH. This seems counter-intuitive, but it allows funds to be put to more use. If you own the 100 ETH, you may want to HODL it and let it appreciate in value. However, you may see an opportunity elsewhere that you don’t want to miss. Therefore, you deposit the 100 ETH, borrow 50 ETH worth of tokens, and put those to work in your new opportunity, for example, to earn interest by providing liquidity to another protocol.

Act as a liquidity provider

Providing liquidity is another way of gaining a yield from deposited funds. In a decentralized exchange (DEX) there are no market-makers who are always available for a buy or sell order, as in a centralized exchange like Binance. Instead, users are incentivized to deposit a pair of tokens, such as DAI and ETH. This allows other users to exchange one of the pair for the other, and they pay a fee to do so. The depositors are known as liquidity providers and receive a portion of the fees. Also, many protocols reserve some tokens when they start out, giving them to liquidity providers in order to get the project off the ground. This is known as liquidity mining. The leading decentralized exchange is Uniswap with a 3 billion USD value locked for liquidity.

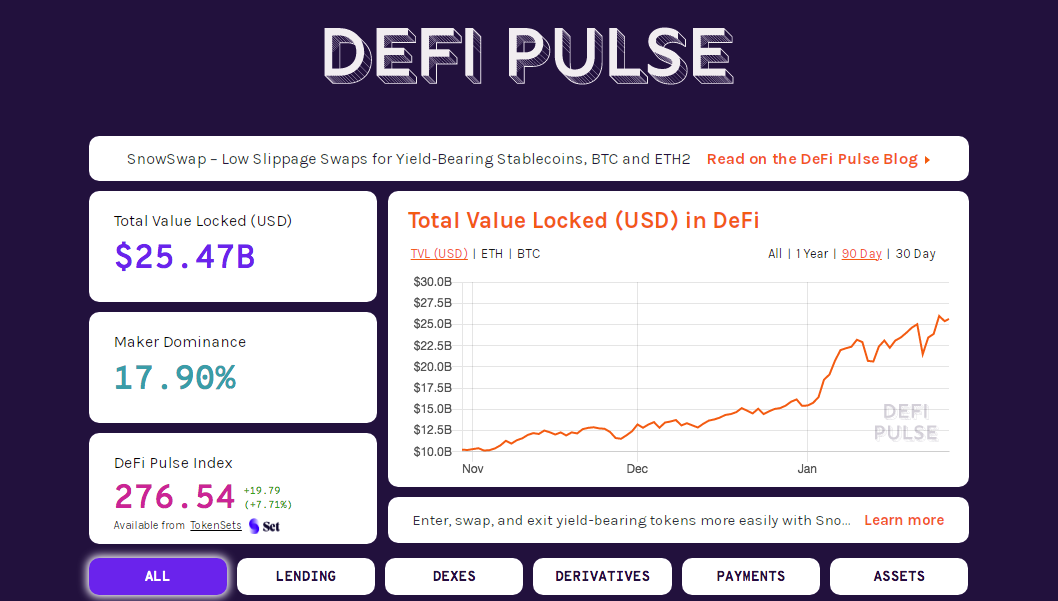

The decentralized finance sector continues to charge full steam as multiple tokens including ETH hit an all-time high and impact the total value locked which grows with the passing of each week currently at 26 billion USD. Ethereum is the main Defi protocol as we have indicated in this article.

Despite these impressive developments, the DeFi sector accounts for just 4,6 % of the total cryptocurrency market capitalization and definitely is primed for explosive growth.

What is the future of DeFi protocols?

Consider this as a brief introduction into the DeFI world with its pluses and minuses like possible hacks, flash loan attacks, rug pulls, etc. This space is definitely new and needs a kind of regulatory adjustment.

In a new opinion piece for the Financial Times, Brian Brooks, the current US Comptroller of the Currency, argues that decentralized finance (DeFi) could pave the way for a kind of “self-driving bank.” With a set of new regulations in place, says Brooks, national bank charters might one day be granted to DeFi protocols.

DeFi protocols are according to him an automated, algorithmically-governed money management systems that essentially skip out on the need for human moderation in financial services and products.

Sources: https://decrypt.co/

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.